I fell in love with a house near the water and almost made a costly mistake. Here’s what I learned about flood insurance, and why skipping it could wash away your biggest investment.

I still remember the day I found the house. It sat on a quiet, winding road, nestled among ancient oaks draped in Spanish moss.

From the back porch, you could glimpse the creek through the trees, a shimmering ribbon of water that caught the afternoon light and promised lazy summer afternoons with a fishing pole and a cold drink. It was the kind of peaceful that made you exhale just by standing there. I wanted it. Badly.

My realtor, ever the steady voice of reason, asked the seller’s agent about the flood zone designation during our initial calls. “Zone AE,” came the reply.

I nodded along, pretending those letters meant something to me. Later, my realtor explained: Zone AE meant the property was in a special flood hazard area. It meant flood insurance wouldn’t be optional, it would be required by my lender.

I remember thinking, *Fine. I’ll buy the insurance. How much could it possibly cost?*

That question, innocent, naive, almost dismissive, sent me down a rabbit hole that would ultimately reshape my understanding of what it means to buy a home near water. And thank God I went down it before I signed anything.

Let me start with what I learned about flood zones, because I had no idea there was a map for this. FEMA creates something called Flood Insurance Rate Maps, which are exactly as boring as they sound until you realize they determine the financial future of your dream home.

These maps divide areas into risk categories. Zone X is moderate-to-low risk. Zone A and Zone V are high-risk areas. The “V” stands for velocity, which means not only can it flood, but wave action can pound your home during storms. That creek I loved? It put me solidly in Zone AE, which is a high-risk area with detailed study behind it.

The first shock came when I got an insurance quote. I had naively budgeted a few hundred dollars a year, the same as my standard homeowners policy. The actual quote was nearly two thousand dollars annually.

For a moment, I almost walked away from the house entirely. How could anyone afford that on top of a mortgage, property taxes, and regular maintenance?

But my realtor, again wiser than me, asked a question that stopped my retreat: “If you don’t buy this house because of the insurance cost, will you regret it every time you drive by?”

That question forced me to dig deeper. I started reading about what happens to homeowners in flood zones who don’t have insurance, or who have insufficient coverage.

I read stories of families watching their life savings wash away because they assumed their standard homeowners policy covered flood damage. Spoiler alert: it doesn’t. Not a single drop.

Flood insurance is a completely separate policy, administered through the National Flood Insurance Program or private insurers, and without it, you are entirely on your own when the water rises.

I also learned that the risk isn’t just about big storms. Sure, hurricanes and major river flooding get the headlines. But the creek behind that beautiful house could rise dramatically from a sudden, slow-moving thunderstorm that parked itself over the watershed for just a few hours.

Flash flooding doesn’t care about your foundation or your sump pump. It finds the low spots, and that house, lovely as it was, sat in one.

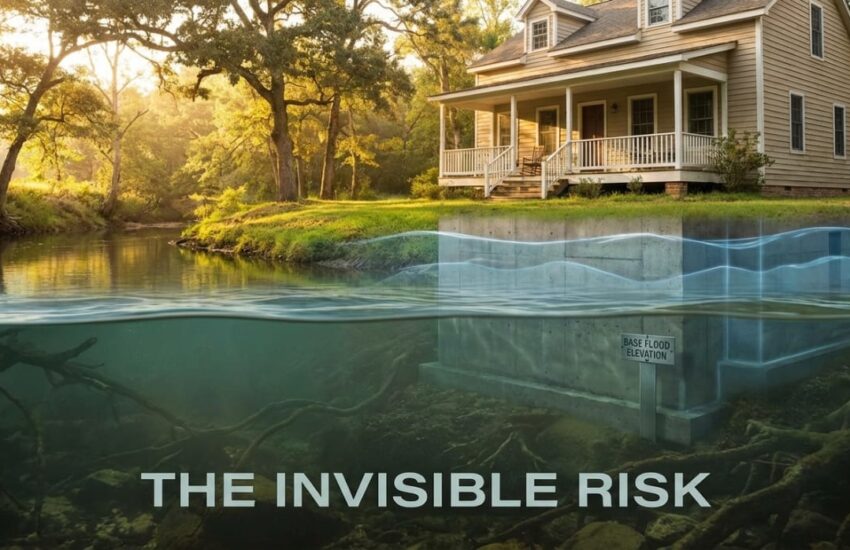

The second shock came when I looked at the elevation certificate. This is a document that shows where your home sits relative to the base flood elevation, the height floodwaters are expected to reach during a base flood event. If your home is below that line, your risk and your premiums go up.

If it’s above, you might catch a break. The house I loved was built in the 1970s, long before modern floodplain regulations. It sat several feet below the base flood elevation. In a serious flood, water wouldn’t just lap at the doorstep. It would be in the living room.

I started asking harder questions. How often does this area flood? What’s the history of claims on this property? Has the seller ever filed a flood insurance claim? The answers were sobering.

The creek had jumped its banks three times in the past twenty years. Not catastrophic floods, but enough to reach the crawlspace, enough to cause mold issues, enough to make life miserable for the family living there.

This is where the conversation shifts from insurance to reality. Flood insurance isn’t just about reimbursing you for damaged drywall and appliances. It’s about survivability. Without it, a single flood event could leave you with a mortgage on a home you can’t live in and can’t sell.

You could be paying for a house that’s essentially a write-off while also trying to find rent money for somewhere else to live. That kind of financial spiral doesn’t just hurt your bank account; it breaks your spirit.

I also learned that even if you’re not in a high-risk zone, flood insurance is worth considering. FEMA estimates that more than twenty percent of flood claims come from properties outside high-risk areas.

Why? Because water finds its way. A blocked culvert, a new development upstream that changes drainage patterns, an unusually intense storm, any of these can turn a “low-risk” property into a disaster zone. And if you’re not in a high-risk zone, your lender won’t require insurance, which means when the flood comes, you’re completely uncovered.

After all this research, I sat down and did the math. Two thousand dollars a year, spread across a thirty-year mortgage, was sixty thousand dollars. That sounds like a lot, and it is.

But against the cost of a total loss? Against the peace of mind of knowing that if the creek rises, I won’t lose everything? It started to feel less like an expense and more like a necessity.

I made an offer on the house. We negotiated, and the seller agreed to credit me part of the first year’s premium at closing. It wasn’t everything, but it was something. And when I finally sat at that closing table, signing papers that made the house mine, I felt something unexpected: relief.

Not just excitement, not just pride, but a quiet, grounded relief that I had gone into this with open eyes. I knew the risk. I had planned for it. I wasn’t pretending the water wasn’t there.

That was three years ago. The creek hasn’t flooded yet, though it’s come close once or twice. Every time the rain starts falling hard, I check the weather, I watch the water level, and I remind myself that insurance isn’t about predicting disaster.

It’s about making peace with uncertainty. It’s about loving a place enough to protect it from the very thing that makes it beautiful.

If you’re looking at a home near water, don’t let the insurance quote scare you away before you understand the full picture. Get the elevation certificate. Talk to an insurance agent who specializes in flood coverage.

Ask the hard questions about the property’s history. And then, with all that information, make your choice. The water will always be there. The question is whether you’ll be ready for it

References

Federal Emergency Management Agency. (2024). *Who’s eligible for NFIP flood insurance?* FloodSmart.gov. Retrieved from https://www.floodsmart.gov/get-insured/eligibility

Fannie Mae. (2026). *Flood insurance requirements for all property types*. Selling Guide B7-3-06. Retrieved from https://selling-guide.fanniemae.com/sel/b7-3-06/flood-insurance-requirements-all-property-types

Legal Clarity. (2025, February 22). *What flood zones require flood insurance?* Retrieved from https://legalclarity.org/what-flood-zones-require-flood-insurance/

Policygenius. (2023, October 11). *Is flood insurance required? Find your lender requirements*. Retrieved from https://www.policygenius.com/homeowners-insurance/do-i-need-flood-insurance/

National Association of Insurance Commissioners. (2024). *Flood insurance*. Retrieved from https://content.naic.org/consumer/flood-insurance.htm